Bonds are back – The Cambridge Weekly

The Cambridge Weekly – 21st August 2023

Bonds are back

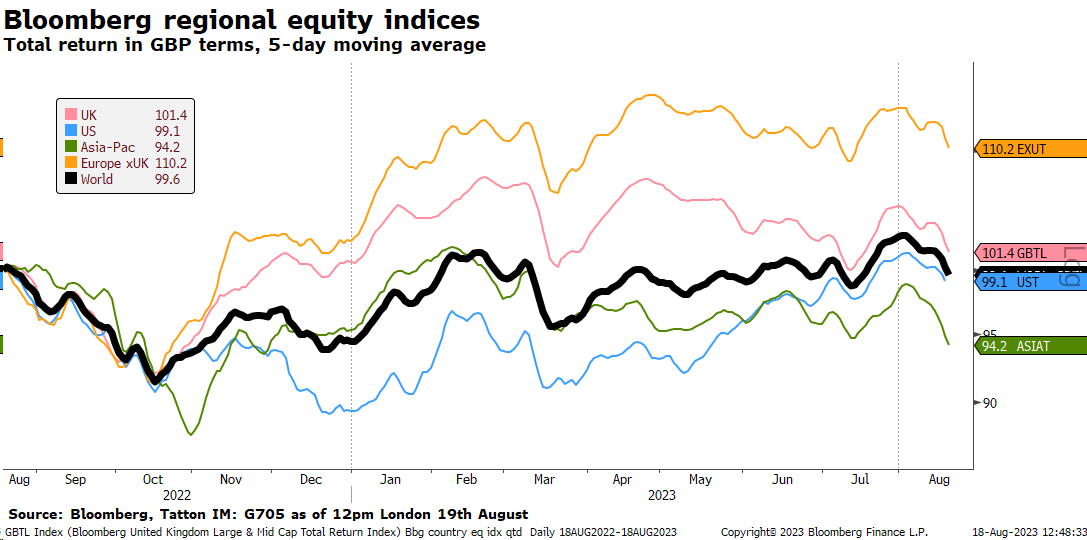

Both equity and bond markets have had another rather difficult week and with it August has mostly erased the positive returns of July. From the medium-term perspective, UK-listed equities are nearly back down to the level at which we started the year. Asia, pressured by Chinese stocks, is about 1% below its January starting point. Overall, world markets are largely unchanged from a year ago.

Perhaps the conclusion one might draw is that markets have not really been doing much. For those of us involved in capital market investment on a day-to-day basis, it can feel as if we are lurching between positive and negative extremes all the time. However, when putting the current moves into a longer timeframe, one can see that moment-by-moment emotions can be misleading.

Nevertheless, last week saw a downturn since our World equity index in the chart above reached its high point at the end of July. Many commentators have pointed to the rise in global bond yields as a big driver of the reverse in sentiment, or at least as the underlying cause of this technical correction , on the basis of a renewed re-rating of equities on the back of higher bond yields. The US 10-year bond yield has risen to a 4.3% high, higher than at any point going back to July 2008. The UK 10-year gilt yield has risen to 4.7%, the highest since June 2008.

At first glance, investors may think the rising yields are building in higher long-term inflation expectations, but this current move does not appear to have been spurred by a worsening inflation backdrop. Inflation expectations – as implied by the pricing of inflation-linked bonds – for the next two to three years seem to have actually fallen back a little.

Therefore, what has changed is the ‘real’ yields, or what is left of a nominal yield of e.g., the 10 -year 4.3% after subtracting the expected rate of inflation. These have become more positive after spending many months (even years) near or below zero. While the topic may sound a little niche to many readers, the level of real yields does matter, and so in the first of our two articles this week we look at the recent movements in real yields and currencies, especially as reflected in the exchange rate of sterling (in the second article, we draw some potential inferences from the weakening Russian rouble while oil prices have moved a little higher).

Rising long-term real yields can be associated with strong growth. The rationale is that an economy that is productive and expanding will provide lots of opportunity, and that will mean companies wanting more capital in order to take advantage of the opportunity – demand for capital that in turn drives up the cost of capital. One can possibly see some evidence of a stronger demand for capital in the US, where bond issuance has increased after a slowdown through last year. At the same time, the US government has stepped up its borrowing programme following the debt ceiling problems earlier this year.

However, this increase in issuance has arrived after institutional investors had already bought a lot of bonds in the first quarter of the year in the expectation that the US Federal Reserve (Fed) would shortly begin to ease monetary policy, therefore locking in what was seen as rates as high as they would probably get during this cycle.

Indeed, since the US regional bank wobbles in March, many investors have thought that an easing of policy was imminent. ‘Imminent’ is only a short period and we are now quite a long way on from there. The release of the minutes from July’s Federal Open Markets Committee meeting last week made it clear that, while they may not tighten for much longer, the next move would probably still be to raise interest rates.

Oddly, the short rates (i.e. on cash) have hardly budged since that July meeting, perhaps not surprising because not much has really changed. Rather, the unwinding of over-extended expectations of what and when the first rate cuts may come after the last rate rise seems to be at play. This rise in US real yields has come at a point when US economic data suggests ever more strongly, reasonable and persistent growth – rather than looming recession which may force rate cuts. That has shifted longer yields to a more normal relationship with shorter rates (although the yield curve which plots this relationship along the maturity band is still inverted), and that in turn has undermined the basis for expensive equity valuations. The longer duration tech stocks in the NASDAQ have been harder hit than most (although the mega-cap ‘Magnificent Seven’ are still holding up, relatively).

So, capital markets appear to be undergoing a rather technical shift, based on the described re-rating on the back of higher-for-longer bond yield expectations, making recently extended expectations untenable, even if the earnings outlook has marginally improved. Given that August is a month with low trading volumes, it could continue to be negative, especially if the momentum trading funds start to add to the flows. However, a little bit of valuation adjustment would be a good thing in the medium term, as it would lower the recent market nervousness as expressed in the continuous up and down since the start of the year.

Turning to the situation at home, at first glance, last week’s UK data was unhelpful. The sharp rise in wages (+8.2% annually when including bonuses, using the rolling three-month averages) looked awfully inflationary, given it is not underpinned by similar levels of productivity improvements. However, just as in the US bond market, the UK inflation expectations component hardly shifted. The employment component in the data showed some unexpected weakness, and this is probably a better indicator of the current situation because it is more indicative of what lies ahead, rather than the rise itself, which reflects the past. Changes in wages are very historical whereas jobs are timelier (even if the whole data set is not a good indicator of current activity). The retail sales data showed weakness which may have been related to wet summer weather but, equally, was in line with recent months when adjusted for inflation.

The two-year rate is about 0.4% below the peak of early July (although it is admittedly still up about 0.3% on the week) while the 10-year rate has regained its early July level. However, UK yields at all levels may be peaking given that financial conditions are tighter here than in the US, and so the backdrop to rising UK yields is arguably less positive than across the Atlantic. The US real yield levels may be sustainable given the investment boost follow-through of the Biden fiscal packages, but there is no comparable fiscal stimulus here. While the UK fiscal deficit is nevertheless set to expand because of the rising interest rate burden, the medium-term fiscal outlook is quite contractionary, or we might even call it austere. That means relatively less issuance and relatively less growth, a situation which may prove to be the healthier policy choice but one which argues for lower bond yields.

UK equities have been hurt both in absolute and relative terms by the outsized rise in yields, but without the US perspective of an improving growth picture – so an end to this difficult situation would be welcome.

As we said earlier, the US rise in yields is at least partly a reflection of an economy which has resilient drivers of growth. So far, despite wobbles, households and businesses have seen rises in income which are not much different to current interest rates. However, some of that resilience may be a result of overconfidence. Markets currently reflect that positivity, and it is possible we could see consumer and business confidence also decline if markets wobble more than currently. If that were to happen, there is the risk the recent virtuous circle environment of resilient growth turns into a vicious circle where a fall in financial risk appetite provokes a fall in economic activity. This ‘wealth effect’ has happened before, most notably in the early part of this millennium. It remains an outside probability, but one which should warn us about being complacent.

Sterling too strong

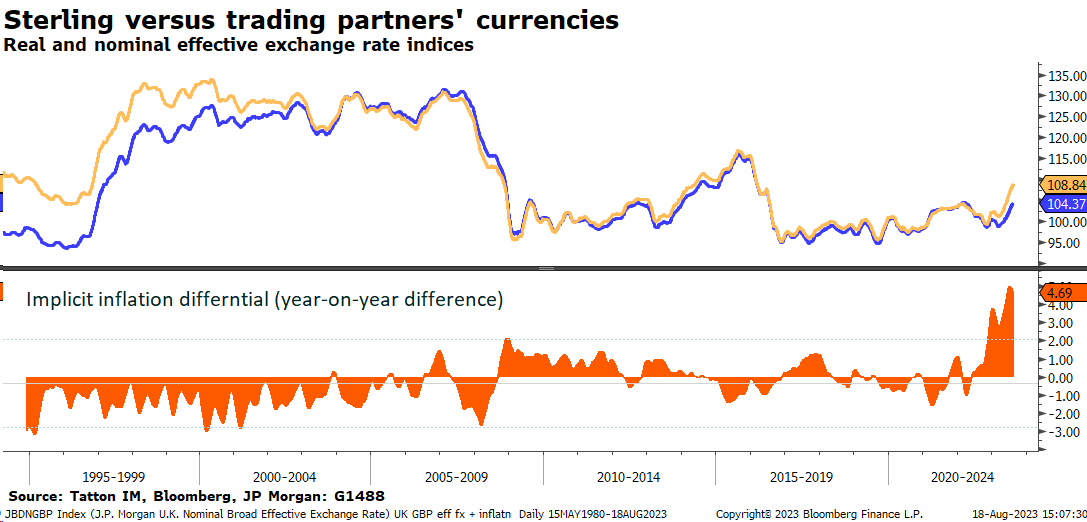

You might be surprised to learn that, on a trade-weighted basis, the best performing major currency of the year so far is none other than our Great British pound. Sterling has gained 5.13% against the UK’s trading partners since the start of 2023. The euro is up just 2.3% over the same period, while the dollar is basically flat (in fact down 0.2%) and Japan’s yen has sunk 8.6%.

Moves in currency values are normally seen as reflecting confidence – or lack thereof – in regional economies. But the commentary around Britain’s economy this year has been nothing but glum. We have had persistently high inflation (now much higher than other countries), and aggressive interest rate rises leading to soaring mortgages and falling house prices. Although the UK has not officially dropped into recession, growth has been effectively zero for over a year.

And yet, sterling has gained against its peers. In fact, that 5% gain is in a sense understated, as it does not take into account varying levels of inflation. UK inflation has infamously been higher than Europe, and significantly higher than the US, which is now just above 3%. As most Britons are well aware, your pound buys you much less than it did, but in terms of foreign currencies, it buys 5% more. Since the UK’s biggest trading partners have not seen as high inflation as here, that means the real effective exchange rate has increased more. This can be seen in the chart below – with the blue line showing the nominal trade-weighted rate and yellow showing the real effective rate.

This is puzzling if one thinks exchange rates should roughly follow purchasing power parity (PPP) rates. As we wrote a few months ago though, consumers’ home bias for purchases means that is almost never how exchange rates work – even over the long term. More important are financial intermediaries, whose job it is to balance the flow of currency against the flow of goods and services. Differences in rates of real (inflation-adjusted) capital return are therefore crucial.

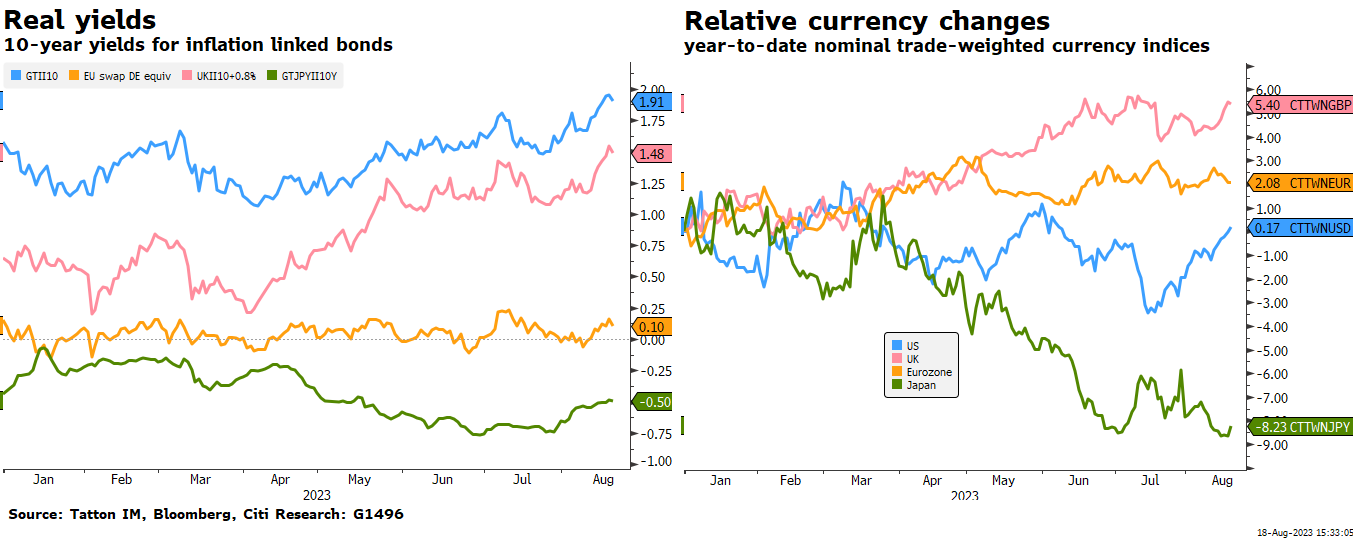

This goes some way to explaining sterling’s strength. After a series of rate rises from the Bank of England (BoE) and the recent fall back in implied inflation expectations, the real yield on 10 -year gilts is now just under 1.5%. Germany’s real yields are still practically zero, and Japanese bonds give a real yield of -0.5%. As it has been for a long time, the US is out in front with a real yield of 1.9% on 10 -year US Treasuries – a reflection of long-term growth expectations.

Should we read the UK’s high real yields as a similar expectation of higher growth? It is possible, but unlikely. If the British economy justified its high real yield in terms of growth, that would imply expectations of substantial long-term profit growth. But this is hard to match with the wider pessimism about the UK economy. More likely, the move up in real yields is a consequence of the BoE’s aggressive stance – necessitated by persistent and UK-specific supply-side problems – together with an extended bond market sell-off. Nominal UK gilt yields are now above where they were during October’s ‘mini budget’ crash, and have risen much more steeply than German yields.

Compare, for example, the UK’s situation to Japan. As shown in the chart below, Japanese real yields (green line in the left hand chart) have moved further negative through the course of this year, matching a sharp decline in its currency value (right hand chart). This could imply a stagnant economy that needs devaluing against its peers – a situation Japan is all too familiar with. But in actual fact, this year has seen huge improvements in the profitability of Japanese companies, and at long last a move away from decades of deflation.

Currency and real yield moves helped create this environment. The sliding yen has made exporters significantly more competitive, boosting profits. Over the past few years, exports (as a percentage of GDP) have gone from around 13% (at the end of 2019) to currently around 18%. Japan’s terms of trade are now much more favourable and, thanks to substantially lower borrowing rates, the relative potential returns in corporate Japan look better than they have for decades. If things carry on as they have, we would expect Japanese assets to appreciate – making the yen look undervalued.

By contrast, the profitability of UK exporters is hurt by sterling strength. A rising pound has helped ease input costs, but Brexit-driven changes mean the goods and services that British consumers buy (which are still overwhelmingly from Europe) are structurally more expensive now than a few years ago. Moreover, the flipside of being able to buy more from trading partners with your pound is that those partners can buy less from you – making British firms less competitive.

This might not be much of a problem if the economy is vibrant enough to handle it. The US saw its currency appreciate dramatically last year, along with a substantial rise in real yields, but this was justified by the relative dynamism of US companies. UK companies arguably need more of a helping hand, but are currently getting the opposite.

The damage to UK profits will probably not be as big as the corresponding benefit to Japan in its opposite case. But it does mean that both UK assets and its currency have become more expensive relative to economic fundamentals. Put another way, sterling looks vulnerable in the medium term. Over the coming months, we might see a slide – particularly against competitive currencies like the yen. The pound is strong now but, unfortunately, this may not be a good thing for the British economy.

Russia struggling to shift supply

Oil traders are feeling bullish. Crude prices are around $5 per barrel higher than a month ago – despite a fairly sizable pull-back last week. In July, international oil benchmark Brent crude was one of the best performing indices, gaining 11.9% in sterling terms. Last week’s jitters came after further economic disappointment in China, but some industry analysts see them as just a hiccup. Thanks to meaningful production cuts from OPEC+ (which includes Russia), predictions of $90 per barrel (pb) or even $100pb are being floated.

That would be quite the turnaround. Brent is a little under $85pb at the time of writing, and has not settled above the $90 mark since mid-2022. Since then, supply side fears have faded, and global demand has become the key concern. Developed markets have slowed, and a few have slipped into recession, while the Chinese economy – so often the main driver of global commodity demand – has severely undershot expectations from the start of this year. Tellingly, during the fall back from 2022 highs, Brent fell below the five-year average price in real (inflation-adjusted) terms.

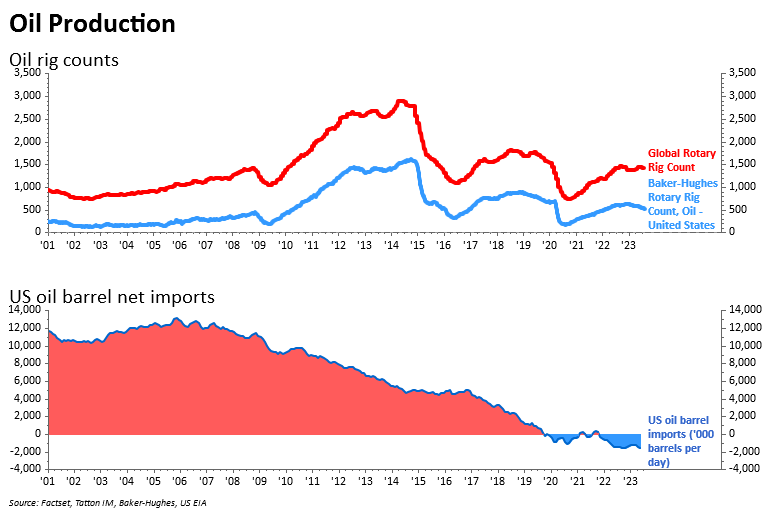

But the decline has been convincingly arrested over the summer. Some of this is down to the surprising resilience of the US economy, and particularly its consumers. However, at most that probably makes up for the continued disappointment in China. And even here, some make the point that China opening up travel actually pushed up oil demand, even if overall economic momentum has been underwhelming. As so often, no price story is complete without looking at the supply side – which has been restricted in the oil market. We have seen production cuts from OPEC+, US shale producers and others – a major variable to explain elevated oil prices.

Saudi Arabia, the world’s largest crude exporter and OPEC’s de facto leader, recently extended its voluntary production cut of 1 million barrels per day to September and noted that cuts may deepen in the future. Russia also promised to export 300,000 fewer barrels per day in September, showing the cartel’s commitment to maintaining high prices. According to one recent survey, the total production output of OPEC+ hit its lowest point since August 2021.

US shale producers have also reined in supply. Production dramatically increased during the post-Covid boom in demand, then jumped again following Russia’s war in Ukraine and the oil supply fears it brought. But the long price slide from last year took a toll on producers’ operating margins – particularly as their own energy costs shot up – leading many to pull back on production. You can see this in the plateauing rig counts in the chart on the next page.

Production cuts are only part of the story, though. If the recent oil price moves were just a case of standard cartel management, you would probably expect to see less intense cuts as prices climbed above $80pb – or even some members breaking ranks for individual gain. This is exactly what has happened through previous OPEC+ agreements, but the Saudis and their allies are not flinching now. And if this was a simple cyclical story, you would not expect to see a sustained uptick in prices while demand was still in a weakening phase.

For us, the most interesting player in this supply tightening is Russia. Despite some near-apocalyptic warnings when Moscow launched its invasion of Ukraine, the aggregate effect of Russia’s war and the ensuing western sanctions on global oil supplies has been relatively small. This was – as widely suspected – down to a rerouting of Russian supply to Asia, most notably the large energy-intensive economies of India and China. That is why, in the early part of last year, Russia’s trade balance (exports minus imports) stayed surprisingly healthy despite its apparent supply cuts.

In the last few months, Russia’s trade balance has deteriorated significantly. This is clear from the slide in foreign currency reserves, which now threatens to bubble over into a full-blown rouble crisis as widely reported in the news this week. Last Wednesday, Moscow hiked interest rates by an extraordinary 3.5% to stop the bleeding, and its finance ministry is reportedly proposing tough capital controls. One of which would force Russian exporters to sell up to 80% of their foreign currency revenue within 90 days of receiving it or risk being banned from government subsidies.

Recently, there have been suggestions that the flow of Russian fuel to Asia has dwindled. This would back up the poor trade balance data – exacerbated by the continued need to import arms. This might suggest that the west’s attempts to dissuade Asian countries from buying Russian oil and gas are finally getting through. Notably, this does not seem to be the case for India, which is willing to pay for Russian oil at a relatively small discount (the Urals blend index is trading at $72pb, well above the west’s $60 price cap). But for China, this may have borne fruit.

The US and China are currently engaged in an increasingly fraught back-and-forth over import restrictions. Underneath this though, both are fully aware how important the flow of goods and services between them – the biggest trade relationship in the world by volume – is. This is particularly true for China, as it struggles with slow growth and deflation. It is very plausible that Beijing might offer to dent Russia’s cashflow to get itself a better deal, and that Washington would accept.

Much of this is speculation, but Russia’s financial troubles are certainly not. It is particularly jarring that the rouble has slid so much while oil prices (including Russia’s discounted offering) have climbed, as the former is unequivocally a petrocurrency. It will undoubtedly mean further pressure on the country’s economy and finances, though as always with Russia the question is whether this pressure reaches the inner circle.

If it does, it could mean ceasefire talks – short or long term – in the near future, though that may be a little optimistic and all too uncertain to predict if rational behaviour is assumed to be the driver. Much more likely is that it could increase friction between Russia and Saudi Arabia over production cuts, with the former needing revenues to fund its damaging war. In either case, oil prices would struggle to go higher over the medium term.

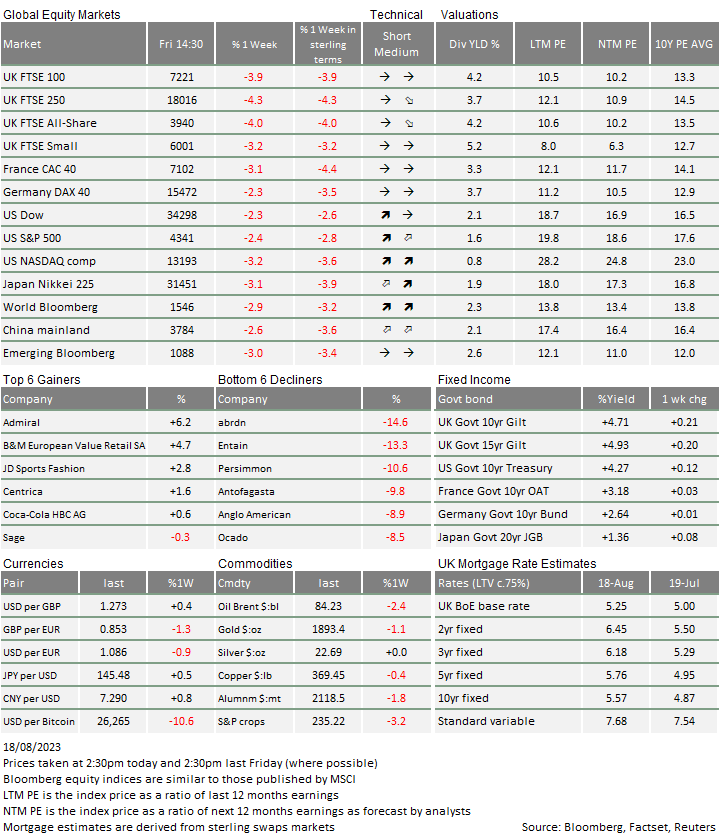

* The % 1 week relates to the weekly index closing, rather than our Friday p.m. snapshot values

If anybody wants to be added or removed from the distribution list, please email enquiries@cambridgeinvestments.co.uk

Please note: Data used within the Personal Finance Compass is sourced from Bloomberg/FactSet and is only valid for the publication date of this document.

This material has been written on behalf of Cambridge Investments Ltd and is for information purposes only and must not be considered as financial advice. We always recommend you seek financial advice before making any financial decision.

Past performance is not a guide to future performance.

The value of your investments can go down as well as up and you may get back less than you originally invested.

Source of financial market data: MorningstarDirect.